The following notations are used in the mathematical definitions and the description of the Intel MKL VSL Summary Statistics functions.

Matrix and Weights of Observations

For a random p-dimensional vector ξ = (ξ1,..., ξi,..., ξp), this manual denotes the following:

-

(X)i=(xij)j=1..n is the result of n independent observations for the i-th component ξi of the vector ξ.

-

The two-dimensional array X=(xij)p x n is the matrix of observations.

-

The column [X]j=(xij)i=1..p of the matrix X is the j-th observation of the random vector ξ.

Each observation [X]j is assigned a non-negative weight wj , where

-

The vector (wj)j=1..n is a vector of weights corresponding to n observations of the random vector ξ.

-

is the accumulated weight corresponding to observations X.

Vector of sample means

for all i = 1, ..., p.

Vector of sample variances

for all i = 1, ..., p.

Vector of sample raw/algebraic moments of k-th order, k ≥ 1

for all i = 1, ..., p.

Vector of sample central moments of the third and the fourth order

for all i = 1, ..., p and k = 3, 4.

Vector of sample excess kurtosis values

for all i = 1, ..., p.

Vector of sample skewness values

for all i = 1, ..., p.

Vector of sample variation coefficients

for all i = 1, ..., p.

Matrix of order statistics

Matrix Y = (yij)pxn, in which the i-th row (Y)i = (yij)j=1..n is obtained as a result of sorting in the ascending order of row (X)i = (xij)j=1..n in the original matrix of observations.

Vector of sample minimum values

for all i = 1, ..., p.

Vector of sample maximum values

for all i = 1, ..., p.

Vector of sample median values

for all i = 1, ..., p.

Vector of sample quantile values

For a positive integer number q and k belonging to the interval [0, q-1], point z i is the k-th q quantile of the random variable ξi if P{ξi ≤ zi} ≥ β and P{ξi ≤ zi} ≥ 1 - β, where

-

P is the probability measure.

-

β = k/n is the quantile order.

The calculation of quantiles is as follows:

j = [(n-1)β] and f = {(n-1)β} as integer and fractional parts of the number (n-1)β, respectively, and the vector of sample quantile values is

Q(X,β) = (Q1(X,β), ..., Qp(X,β))

where

(Qi(X,β) = yi,j+1 + f(yi,j+2 - yi,j+1)

for all i = 1, ..., p.

Variance-covariance matrix

C(X) = (cij(X))p x p

where

Pooled and group variance-covariance matrices

The set N = {1, ..., n} is partitioned into non-intersecting subsets

The observation [X]j = (xij)i=1..p belongs to the group r if j ∈ Gr. One observation belongs to one group only. The group mean and variance-covariance matrices are calculated similarly to the formulas above:

for all i = 1, ..., p,

where

for all i = 1, ..., p and j = 1, ..., p.

A pooled variance-covariance matrix and a pooled mean are computed as weighted mean over group covariance matrices and group means, correspondingly:

for all i = 1, ..., p,

for all i = 1, ..., p and j = 1, ..., p.

Correlation matrix

for all i = 1, ..., p and j = 1, ..., p.

Partial variance-covariance matrix

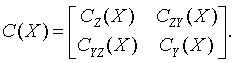

For a random vector ξ partitioned into two components Z and Y, a variance-covariance matrix C describes the structure of dependencies in the vector ξ:

The partial covariance matrix P(X) =(pij(X))kxk is defined as

where k is the dimension of Y.

Partial correlation matrix

The following is a partial correlation matrix for all i = 1, ..., k and j = 1, ..., k:

where

-

k is the dimension of Y.

-

pij(X) are elements of the partial variance-covariance matrix.